How to consolidate pensions – The Telegraph

Ava White

Published Apr 08, 2026

Keeping track of your retirement savings is not always easy, especially if you have joined several workplace pension schemes over the years. Knowing how to consolidate pensions in one plan can make it easier to manage your savings.

Industry reports have already highlighted the need for and benefits of pension consolidation. The Lost Pensions Survey, published by the Pensions Policy Institute, revealed that in 2022 the total value of assets held in lost or forgotten pensions in the UK stood at £26.6 billion.

In addition, a Financial Conduct Authority paper shows that 89 per cent of all individual personal pensions are in schemes that are closed to new business, and some £250 billion of assets held in those schemes might benefit from pension consolidation.

Here is a guide to how to consolidate pensions and whether doing so would be a good idea for you.

- Have you lost track of a pension from an old employer? Combine old pensions with ease via the Telegraph Media Group Pensions Service*

What is pension consolidation?

Pension consolidation is the process of combining multiple pension pots into one scheme or retirement savings product. Many people choose to do this to help them manage their retirement savings and track their progress more easily.

Many of us work for several different employers during our careers, often joining each new company’s workplace pension scheme every time we change jobs.

That can mean an awful lot of paperwork to stay on top of and a lot of wondering what to do with multiple pensions. This can be even more time-consuming if you have also paid into personal pensions.

Should I get all my pensions in one place?

Before asking how to consolidate pensions, the first question you should consider is “Should I combine my pensions?”

Combining pension pots can make it much easier to monitor how your money is invested and to keep charges to a minimum. You will also receive only one pension statement a year, so you can easily understand how your investments are performing.

Having your retirement savings in one place may also make things simpler for you when you reach retirement, as you will only have to decide how to take an income from one pension pot.

However, it is vital to consider whether you will be sacrificing important benefits and/or incurring charges if you transfer. So if you have several pensions and you are not sure whether consolidating them is the right choice for you, read on to find out more.

Pros and cons of pension consolidation

How to make your decision

Check your charges

If you are considering transferring a defined contribution pension, check how much you are paying in charges. Often older pensions have steeper charges, so you may be able to save by transferring your pension to a cheaper plan. If the fees you are paying are higher than 1 per cent, you are almost certainly paying more than you should.

Check for exit penalties

Some pensions charge an exit penalty if you want to move your money elsewhere, so if one of yours does, you need to establish whether it’s worth transferring your pensions into one plan, or if the costs will outweigh the benefits.

Profile Pensions, providers of The Telegraph Media Group Pension Service, can check for any exit penalties and notify you if any of them is over £50.*

Check your pension performance

It is also worth looking at your pension performance. If one or more of your pension plans has produced underwhelming returns relative to others you hold, it could be time to transfer your savings to a different pension or change the investments within the underperforming pension.

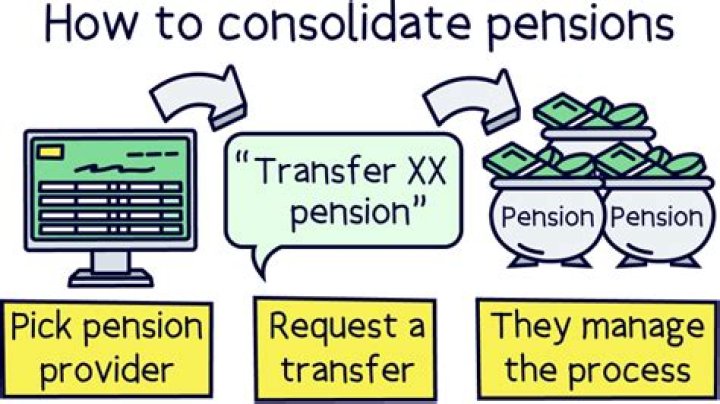

How to consolidate your pensions

Once you’ve decided that consolidating your pensions is the right decision for you, the steps to combining them are easy.

Get a personalised pension plan and start a new pension, with funds chosen specifically for you

Transfer any old pensions into your new pension or get help tracking down any lost pensions

Monitor your new pension securely online, informing your pension company of any changes to your circumstances or personal details

The Telegraph Media Group Pensions Service, provided by Profile Pensions, is designed to help you consolidate defined contribution pensions into one place and provides investment advice tailored to your circumstances. When you sign up you will be allocated a dedicated pension adviser to discuss your pension investments with.

Combining different types of pension

It’s also important to be aware that different types of pension will have an impact on whether consolidation is possible, or even a good idea.

If any of your pensions are defined benefit plans, such as a final salary pension, these could offer valuable benefits that could be worth keeping. Combining defined contribution pensions is usually more straightforward. With this type of pension, the amount you will end up with at retirement depends on the size of the contributions, and how the investments these have gone into have performed.

Example 1

Mr Smith is considering pension consolidation. He has two small defined contribution pensions with high fees and one defined benefit pension.

After he answers some initial questions from Profile Pensions about what he wants from his pension and his retirement, Mr Smith receives a personalised pension plan identifying the best funds for him out of the 40,000 regulated funds on the entire market and where his money will be invested.

He decides that the fees he is paying on his defined contribution pensions are too high, and it would be worthwhile moving those investments into a new modern scheme.

Because one of his pensions has a defined benefit, Profile Pensions suggests he doesn’t move that one, but the other two are combined into one easy-to-manage pension plan with lower fees and more flexibility.

Mr Smith can now easily and quickly monitor his new pension in a secure, online account and make any changes, set up contributions, transfer any other old defined contribution pensions or draw down funds when he reaches retirement age.

Example 2

Mrs Jones asks “How do I get all my pensions in one place?” She has three pension pots, all from the NHS or other Government bodies. After speaking to their team, Profile Pensions explains to her she is unlikely to benefit from pension consolidation because she could lose valuable guarantees. In fact, she may not be able to transfer her old pensions at all and may be legally obliged to seek independent financial advice.

FAQS

Can I have more than one pension?

Yes, there is no limit to how many pensions you can have. This includes all types of pension, including workplace, private and defined benefit pensions. You can also pay into more than one pension at the same time and on most pensions there is no limit on how much you can pay in. However, there is a limit on how much you can receive tax relief on.

It may be beneficial to keep multiple pension pots if you have defined benefits or are currently enrolled in a workplace pension. However, there may be advantages to combining other pensions you have. By consolidating your savings it can be easier to monitor performance and fees and to manage any changes to your details, for example when you change address.

Can you pay into two pensions at the same time?

You can pay into as many pensions as you like but your tax relief allowance will remain capped at 100 percent of your earnings or £60,000 per year (whichever is lower), across any pensions you are paying into. So you would only receive pension tax relief up to that amount, if you’re eligible.**

How long does pension consolidation take?

This can vary and depends on your old pension providers and how quickly they can process your request and complete the transfer, as well as whether they can process it electronically or by post. This could be anything from a few weeks to a few months. Your new or old provider should let you know if you need to do anything for the transfer to happen and this can also affect the speed of combining your pensions.

While your pension funds are being invested, they will be out of the market for a short time while the transfer takes place. But your new pension provider will let you know when the consolidation is complete.

What is the best way to consolidate pensions?

It will be easier and faster for you to use a pension company that can combine any old pensions for you, including contacting your old providers on your behalf, rather than attempting it yourself.

You can consolidate multiple pension pots without the hassle via The Telegraph Media Group Pension Service. Provided by Profile Pensions, this service is designed to help you track down your old personal and workplace pensions*, and combine them into a new personalised pension plan.

After answering just a few simple questions, you will receive an impartial personalised pension plan with a tailored investment strategy – selecting the best investments for you from 40,000 regulated funds. You can then easily add pensions you know about/find your old pensions* and transfer them to your new plan all in your secure online account. You will even be allocated a dedicated Pension Adviser who you can contact directly to discuss your recommended plan or to ask any pensions questions.

There is no cost to transfer old pensions you know about into your new personalised pension plan. However if you want help to track down pensions you have lost track of or would like your old pensions checked for any guarantees, benefits, or exit penalties worth £50 or over then there is a fee of 1% of the pension pot value, (taken at the point of transfer) to use this service.

Sign up today to combine your pension pots with the Telegraph Media Group Pensions Service

Read more:

*If you want to track down pensions you have lost track of then there is a fee of 1% of the pension value taken at the point of transfer. As part of their “Find, check and transfer” service Profile Pensions will also check the pensions they find for you and identify any exit penalties or guarantees worth over £50, so you can be confident that you can make an informed decision about transferring or consolidating these pensions.

**Your annual allowance might be lower if you have: a) flexibly accessed your pension pot or b) a high income

Capital at risk. Past performance is not a guide to future performance. This website does not constitute personal advice. If you are in doubt as to the suitability of an investment, please contact one of Profile Pensions’ advisers. Prevailing tax rates and reliefs are dependent on your individual circumstances and are subject to change.

Telegraph Media Group Limited is an Introducer Appointed Representative of Profile Pensions, a trading name of Profile Financial Solutions Limited, which is authorised and regulated by the Financial Conduct Authority. FCA Number 596398. Registered in England & Wales, Company Number 07731925. Registered office address: Norwest Court, Guildhall Street, Preston PR1 3NU.

Information correct at date of publication.

The above article was created for Telegraph Financial Solutions, a trading name of The Telegraph Media Group. For more information on Telegraph Financial Solutions click here.